Ashtead Technology Holdings - Deep Dive

Can Ashtead’s Subsea Fleet Weather the Offshore Wind Stall

Having monitored several recent discussions regarding Ashtead Technology (AT.L), the company has warranted a closer look. After evaluating the current business model and market conditions, my position is one of caution. At present valuations, the stock does not represent a compelling entry point due to significant headwinds and 'macro' uncertainties within the offshore renewable sector. However, should sector sentiment shift, Ashtead’s operational scale makes it a premier candidate for a cyclical turnaround

To the uninitiated, Ashtead Technology (AT.L) might look like just another service provider caught in the wake of energy giants. But if you strip back the balance sheet, you find one of the most aggressive, high-margin players in the complex ecosystem beneath the ocean’s surface.

With the stock trading significantly down from its 2024 highs, the question for every “Deep Value” investor is simple: Are we looking at a high-quality compounder temporarily on sale, or a cyclical “roll up” story about to hit the reef?

The Business: Who Are They?

In an environment where the pressure is crushing, visibility is zero, and a single mistake costs millions, Ashtead Technology doesn’t do the drilling or the building. They rent the tools that make it possible.

Think of them as a hightech “United Rentals” for the underwater world. They own a fleet of over 23,000 specialized assets used in the harshest environments on Earth. Their operations are divided into three critical pillars:

Survey & Robotics: The “eyes and ears” under the sea. They provide the sonar, sensors, and positioning equipment for Autonomous Underwater Vehicles (AUVs) and ROVs.

Mechanical Solutions: The “hands.” Heavy duty tools for cutting, cleaning, and dredging subsea structures.

Asset Integrity: The “doctors.” Equipment used to monitor the structural health of pipes and platforms to prevent catastrophic failure and ensure regulatory compliance.

The Revenue Model: High Stakes, Higher Margins

Ashtead’s profitability and its primary risk stems from its rental-centric model.

Operating Leverage: When Ashtead buys a piece of equipment, the cost is fixed. In a booming market, that asset can be rented out at daily rates that cover the entire purchase price in a matter of months. This is why the company reports “headline” EBITDA margins exceeding 30%.

The Outsourcing Moat: Tier 1 contractors (like Subsea7 or TechnipFMC) prefer to rent rather than own. Why? Because it keeps their balance sheets “light” and ensures they always have the latest technology without the risk of obsolescence. Ashtead takes the “Asset-Heavy” risk, but in return, they capture the “Alpha” of high utilization.

The Service “Hook”: They don’t just drop off a box of tools. They provide the technical calibration and support personnel. This creates high switching costs for the customer; you don’t change your sonar provider mid mission.

The Industrial Backdrop: The Green Mask

Management is quick to highlight their exposure to Offshore Wind, which now accounts for approximately 26% of revenue. However, a cold look at the numbers tells a different story: Oil & Gas remains the engine (74%).

Ashtead is currently riding two distinct cycles:

The Maintenance Cycle (Brown Energy): Aging oil platforms in the North Sea and elsewhere require constant monitoring and eventual decommissioning. This is the “bread and butter.”

The Growth Cycle (Green Energy): The installation of offshore wind farms requires many of the same tools. This has been the primary driver of the stock’s recent “growth” multiple.

The Warning: “The Rental Trap”

From a Deep Value perspective, we must remain skeptical. The rental model is a double-edged sword. When utilization is 90%, Ashtead is a cash-printing machine. If utilization drops to 60% due to project delays which we are currently seeing in the offshore wind sector the bottom line collapses because the fixed costs of maintaining that £100m+ fleet do not go away.

Furthermore, much of the recent growth has been inorganic. Through a “roll-up” strategy, Ashtead has been buying smaller competitors (like Seatronics and Martech) to consolidate the market. In the next section, we will investigate whether they are buying high-quality earnings or simply using debt to mask a slowdown in organic growth.

Industry Dynamics and the Cyclical Straitjacket

To understand Ashtead Technology, one must understand the environment it inhabits: the cold, high-pressure, and prohibitively expensive subsea floor. This is an industry governed by the CAPEX (Capital Expenditure) cycles of energy giants. When Shell, BP, or Ørsted breathe, Ashtead either thrives or suffocates.

1. The Industry Structure: A Tale of Two Energies

The subsea services market is currently undergoing a structural split.

The “Old” Guard (Oil & Gas): This is the foundation. The North Sea, the Gulf of Mexico, and West Africa have thousands of kilometers of aging pipelines and hundreds of platforms. Regardless of the oil price, these assets must be inspected and maintained to avoid environmental disasters. This provides Ashtead with a “floor” of demand.

The “New” Frontier (Offshore Wind): This was supposed to be the infinite growth engine. However, offshore wind is essentially a “packaged interest rate play.” Because these projects have massive upfront costs and long payback periods, high interest rates have turned many “Green Dreams” into “Financial Nightmares.”

2. The Competitive Landscape: A Commodity in Disguise

Ashtead likes to frame itself as a technology leader. From a cold, analytical perspective, that may be a stretch. Ashtead is a logistics and balance sheet play.

Fragmented Rivals: The market is populated by a few large players and many smaller niche rental shops.

The James Fisher Warning: James Fisher & Sons (FSJ) serves as the “ghost of Christmas future.” Their failure to manage a sprawling, debt-funded subsea portfolio shows how quickly margins can evaporate when a company loses its focus.

Low Barrier to Entry, High Barrier to Scale: Anyone with a few million pounds can buy a sonar unit and rent it out. However, few can match Ashtead’s global footprint. The “Moat” here isn’t the technology it’s the inventory availability. If a Tier-1 contractor needs 50 sensors in Angola tomorrow, only a few companies have the scale to deliver.

3. The Cyclical Challenge: The “Peak Utilization” Trap

The biggest risk facing Ashtead today is Mean Reversion.

In the rental business, your “Operating Leverage” is a double-edged sword. When the industry is at its peak, every piece of equipment is out in the field, and margins soars. Investors see these margins and assume they are permanent. They are not.

The Cyclical Red Flags:

Project Delays: We are seeing a global “pause” in offshore wind auctions. When projects are delayed, equipment sits in the warehouse. A warehouse full of idle sensors is a liability, not an asset.

The Capex Cliff: If Ashtead buys £50m worth of new equipment at the top of the cycle, and the market turns, they are stuck with depreciating assets and the debt used to buy them.

The Organic Stall: In their latest reports, Ashtead’s organic growth (growth without acquisitions) slowed to a crawl. This is the classic signal that the cycle has peaked. When you can no longer grow by doing more business, you are forced to grow by buying your competitors usually at the exact moment they are most expensive

Competitive Moat: Does it exist?

If you ask the CEO, he will tell you about “unique technical expertise.” If you ask an objective analyst, the moat is switching costs and reliability. In subsea operations, the cost of the rental equipment is tiny compared to the cost of the ship and the crew (which can be $100k+ per day). A contractor will pay a premium to Ashtead because they trust the equipment won’t break. If the tool fails, the project stops. This gives Ashtead some pricing power, but it is limited by the fact that their competitors (like the newly restructured Acteon units) provide the exact same hardware.

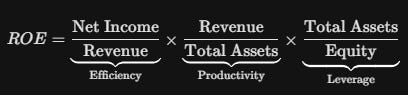

Part 4: The Financials

To the casual observer, Ashtead Technology’s Return on Equity (ROE) the measure of how much profit a company generates with the money shareholders have invested looks spectacular. But as investors, we must ask: Is this profit driven by operational genius, or is it a byproduct of debt and “cycle-peak” luck?

1. The DuPont Dissection: Peeking Under the Hood

To find the answer, we use the DuPont Analysis. Think of this as a “Financial X-Ray” that breaks one big number (ROE) into three smaller, more telling parts.

Lever 1: Profit Margin (Efficiency): Ashtead currently keeps about 16–18 cents of every dollar they earn. This is high, but it’s a “cycle-peak” number. In a rental business, when the market cools, these margins don’t just dip they evaporate because the costs of owning the machines (depreciation) stay the same.

Lever 2: Asset Turnover (Productivity): Ashtead’s turnover is low (approx. 0.5x). This means they have to own a massive amount of expensive “metal” to generate their sales. It is a capital hungry business. If they stop buying new gear, the growth stops.

Lever 3: Financial Leverage (The Multiplier): Ashtead has used debt to buy its competitors. Debt acts like a magnifying glass: it makes the returns look much bigger when times are good, but it magnifies the losses when the market turns.

The Verdict: Ashtead’s high ROE is not coming from working their machines harder (Productivity); it’s coming from borrowed money (Leverage) and high prices (Margin).

Part 5: Meet the Management – Architects of the Roll-up

In a “Deep Value” analysis, the management team is either the guardian of shareholder capital or the primary threat to it. For Ashtead Technology, the leadership is a seasoned team of industry veterans who have successfully navigated the transition from private equity ownership to the public markets. However, their strategic DNA is built for aggressive consolidation, which raises questions about their suitability for a stagnant or declining market.

Allan Pirie: The Tenured CEO

Allan Pirie has been at the helm since 2012, providing a level of continuity rarely seen in the mid cap subsea sector. Under his leadership, Ashtead has transitioned from a niche rental shop to a global “supermarket” of subsea tools.

The Right Fit? Pirie is undeniably an expert in subsea logistics. He has successfully integrated multiple acquisitions and maintained high EBITDA margins during a period of market expansion.

The Risk: Having led the company through a decade of growth, there is a risk of “cyclical blindness.” A CEO accustomed to expansion may struggle to pivot to a “harvest” or “defensive” mode where capital preservation must take priority over top-line growth.

Ingrid Stewart: The M&A Architect

CFO Ingrid Stewart, who joined in early 2021, is perhaps the most critical player in the current “Roll-up” narrative. With a background at Deloitte and Simmons & Company, and nearly a decade as Corporate Development Director at EnerMech, her expertise is precisely in M&A and post-merger integration.

The Right Fit? If the goal is to continue consolidating the fragmented subsea market, Stewart is the ideal CFO. She understands how to structure deals and manage the debt facilities required to fund them.

The Risk: In the world of Deep Value, an M&A-focused CFO can be a red flag. Her background suggests a bias toward “Inorganic Growth.” When the “deal flow” stops or become too expensive due to rising interest rates, the CFO must be able to manage a lean, organic business a skill set distinct from deal-making.

Skin in the Game: Alignment or Agency?

As of early 2026, insider ownership presents a mixed signal for the “Margin of Safety” investor.

CEO Holding: Allan Pirie holds approximately 1.66% to 1.7% of the company’s issued share capital (valued at roughly £4M). While this is a significant personal stake, it is relatively small compared to the 87% institutional ownership.

Compensation Structure: A significant portion of executive compensation often exceeding 75% is tied to performance-related bonuses and equity incentives. While this aligns management with the share price, it creates a “perverse incentive” to pursue short-term earnings growth (often via acquisitions) to trigger bonus thresholds, even if those acquisitions carry long-term risks.

The Institutional Influence: With nearly 90% of the stock held by institutions like abrdn, Schroders, and BlackRock, the management functions more as agents for large funds than as owner-operators. They are under immense pressure to deliver the “growth” that these funds demand, which can lead to over-extending the balance sheet at the top of the cycle.

The Verdict on Management: This is a high-caliber team for an expansionary cycle. They are "deal-makers" by trade. However, for a Deep Value investor, the lack of substantial, founder-level "skin in the game" means we must remain vigilant. If the M&A engine stalls, we will see whether this leadership can pivot from builders to protectors of value.

Part 6: The Ultimate Verdict – Bull vs. Bear

The market has recently punished Ashtead Technology (AT.), but a lower price does not always equal a bargain. We must distinguish between a temporary “dip” and a fundamental shift in the company’s risk profile.

The Bull Case (The Management’s Narrative)

Consolidation Alpha: Ashtead is the dominant “roll-up” player in a fragmented industry. By acquiring competitors like Seatronics, they achieve economies of scale and pricing power that smaller shops cannot match.

Energy Transition Tailwinds: While O&G provides the “floor,” offshore wind is the “ceiling.” The transition to renewables provides a decade-long runway for growth.

Operating Leverage: In a tight market, 28% EBITA margins are sustainable because the cost of the rental fleet is fixed while rental rates are rising.

The Bear Case (The Analyst’s Warning)

Organic Growth Failure: In H1 2025, organic growth (excluding acquisitions) collapsed to 1.3%. This suggests the core business is stagnant, and management is using debt-funded acquisitions to mask a lack of internal momentum.

The Goodwill Anchor: Nearly 45% of total equity is currently tied to Goodwill and Intangibles. In a cyclical downturn, these “assets” are subject to catastrophic impairments that could wipe out the company’s book value.

The CAPEX Treadmill: To maintain a 24% ROIC, Ashtead must constantly reinvest millions into a depreciating fleet. This is not a “capital-light” software business; it is a heavy-industry equipment play masquerading as a high-growth tech stock.

My final conclusion: PATIENT ACCUMULATION

The 40% draw down has removed the “froth,” but it has not yet created a “screaming buy.”

The “Bull” Trigger: If the company can prove in the next two quarters that organic growth has returned to >5%, the current price is a steal.

The “Bear” Trigger: If interest rates stay high and the offshore wind “pause” turns into a “cancellation,” the debt used for the Seatronics deal will become a major drag.

My Final Take: Do not chase the “Green Energy” narrative. Buy Ashtead for its O&G maintenance floor and its asset replacement value. The stock is currently in “No Man’s Land” too expensive for a value investor, and too slow for a growth investor. The best strategy is to wait for the institutional “forced selling” to finish. Once the stock yields 10% on a Free Cash Flow basis (roughly at the 265p level), the risk-reward profile shifts heavily in your favor.

Ashtead still looks cheap at these levels to me

Great read!

First things first, I love your subtitles man. In my writing, I bounce between creative ones like yours and simple ones like "The Industry". Investing can be a deary topic. Thank you for being some flair into it in your own way.

I like how you get at the heart of the business model and industry. I know Ashtead; I come across the stock 7 years ago and the capital requirements put it in the "too hard" bin for me. It's definitely not a technology company.