GigaCloud Technology Inc

The Tariff Trap: As Trade Tensions Heat Up, GCT 'Achilles' Heel' Might Be Your Best Buying Opportunity of 2026

January 19,

Company name: GigaCloud Technology Inc.

Ticker: GCT

Market cap: $1.50B

Stock price: $40.41

The past week has indeed been quite eventful in terms of politics. With all this talk of Greenland and the looming threat of trade war between Europe and America, we are in all likelihood headed towards volatile markets. It got me thinking of a stock on my watch list: this stock is an absolute blazer; it’s up 90% in the past year alone, but might finally have found its Achilles’ heel in these new trade policies

I am talking about GigaCloud Technology Inc.

I think GigaCloud could see some volatility due to the current tariff talks, and if that happens, i think this will be worth having a look at!

Now lets take a look into GigaCloud!

1. Corporate Mission and Revenue Model Overview

GigaCloud Technology (GCT) has made its presence felt as a pioneering force in the area of end-to-end B2B e-commerce worldwide, particularly designed for the “large parcel” products industry. The relevance of the company as an important player in the marketplace is its proprietary solution in the form of Supplier Fulfilled Retailing (SFR) technology, acting as a niche solution for the “empty air” problem, which refers to the natural inefficiency in the logistics for bulky goods, resulting from the non-standardized size, impacting the usage capacity in shipping containers and storage units.

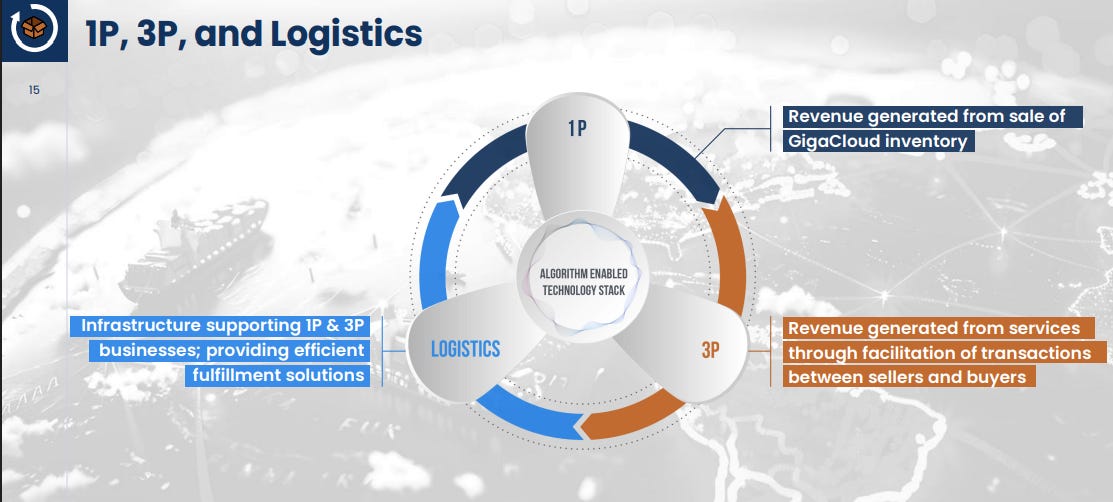

GCT’s financial framework is founded on the following three complementary sources of revenue:

GigaCloud 3P: Service-based revenue generated from facilitating transactions between third-party sellers and buyers within the GigaCloud Marketplace.

GigaCloud 1P: Product revenue generated by selling its owned, procured inventory.

Off-Platform E commerce Revenue: Revenue generated by physical products using third-party giants like Amazon, Walmart, or Wayfair for the purpose of selling products.

The “Money Engine” and Competitive Alpha

GCT operates as a specialized “Money Engine,” delivering a strong “alpha” over and above the industry standard carriers such as UPS and FedEx by harnessing the power of its “Efficiency King” business model:

Aggregation of Fragmented Demand: With over 1,230 active 3P sellers, GCT is able to achieve packing densities and container utilization factors not feasible for individual manufacturers as standalone entities.

Logistics Specialization: For standard parcel carriers, “oversize” fees are typically charged for heavy or cumbersome products. GCT’s system of 35 fulfillment centers and 10.9 million square feet is designed for racking and handling heavy items.

Efficiency Arbitrage: In Efficiency Arbitrage, the firm locks in the value of the large cost disadvantage of piecewise, unmanaged logistics versus the lower unit costs made possible by the integrated high-density physical network.

2. GigaCloud 3P: The Service Revenue Infrastructure

The 3P section describes GCT’s aspiration to be the “Price Boss,” and the operational glue that retains sellers within the ecosystem. Though currently categorized as an “Efficiency King” owing to its cost-based advantages, the 3P infrastructure enables end-to-end fulfillment that allows Asian manufacturers to establish a western retail presence without capital-intensive investment in proprietary overseas logistics.

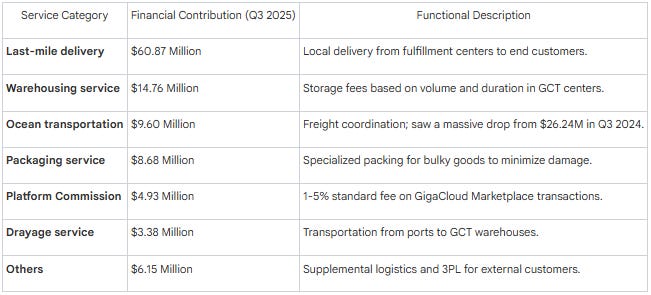

Q3 2025 3P Service Revenue Breakdown:

Through three months to September 30, 2025, total service revenues reached $108.4 million, down marginally 1.8% year-on-year from $110.3 million in Q3 2024. This contraction was largely fueled by the normalization of global freight rates.

The Evolution of Accounting in the Final Mile of Delivery

The key driver in the 3P business remains the last-mile delivery service, which generates $60.87 million in Q3 of 2025. GCT started the first quarter of 2025 by voluntarily adopting a change in its accounting principle to report the final mile transportation of goods as a separate performance obligation. The main reason for adopting the above change in its accounting principle is associated with the development of the marketplace features that offer additional flexibility to customers to select the mode of transportation of goods.

Physical Scale Moat and Use of 3PL Strategies

GCT employs “excess fulfillment capacity” in providing its customers 3PL services. This is done to maximize utilization of its 10.9 million square foot floor space. The network has operated as a major barrier to entry. The “Pain of Exit” is high because it is very expensive to relocate heavy products from GCT’s pallet racks to its competitor.

3. GigaCloud 1P: Internal Product Revenue Optimization

“1P” segment: This is a tool that is utilized for market seeding and market velocity creation in the marketplace. By merchandising their own goods, GCT is able to optimize a private data set for demand insights and demonstrate demand viability within new geography for new sellers in the marketplace.

Growth Resilience and Catalog Depth

For Q3 2025, 1P revenue came in at $98.3 million, a 2.6% increase over the $95.8 million recorded for the same period of 2024. It is significant that the 1P business was relatively more resilient than the 3P service business, which declined by 1.8% for the quarter.

The 1P Strategic Advantage:

1. Market Setup: Demand testing in a market like Germany or Canada using 1P inventory prior to engaging 3P partners.

2. Category Depth: GCT has over 20,000 1P SKUs (Stock keeping unit), making the cumulative marketplace catalog surpass the 50,000 mark as of September 2025.

3. Logistics Insights: By directly managing inventory, GCT is able to maximize container shipping density and warehouse functionality utilizing internal real-world data.

4. Off Platform E-commerce - Off Platform

GCT holds a “channel-agnostic” position, guaranteeing its products are accessible through all major third-party e-commerce channels. It is an important part of growing their volumes to qualify for competitive tier-one ocean freight prices.

Financial Mechanics: B2B vs B2C

GCT defines two off-platform business models which use different accounting methods:

• Product Sales to Business: Selling directly to retail outlets such as Wayfair, Walmart, and Home Depot.

• Product Sales to Consumer: Direct to consumer sales through GCT-owned retail stores on market places such as Rakuten and Amazon.

Off-Platform Revenue increased substantially in Q3 2025 at $125.8 million from $97 million in Q3 2024. This is indicative of GCT’s ability to remain relevant in retail even apart from its own B2B marketplace.

Financial Analysis Report:

1. Revenue Architecture & Growth Path

GigaCloud Technology (GCT), in its continued affirmation of its Supplier Fulfilled Retailing (SFR) business, registered total revenue of $927.2 million for the nine months ended September 30, 2025, marking an increase of 7.2% from the same period in the preceding year. The principal contributory factor in this growth trend has been the company’s “channel-agnostic business approach.” The internal marketplace business has been steadily increasing, but off-platform e-commerce sales (sales through Amazon and Wayfair, among others), which grew by an astonishing 12.8% to reach $353.4 million, were the most remarkable phenomenon.

2. Strength of Balance Sheet and Capital Efficiency

GCT sports a “fortress” balance sheet, highlighted by zero debt and a formidable cash position of $334.8 million (versus $259.7 million at year-end 2024). Liquidity is further supported by an undrawn $30 million credit facility.

Strategically, the balance sheet reflects a “Physical Scale Moat.” While GCT carries $461 million in lease liabilities, this accounts for 10.9 million square feet of specialized warehouse space. This acts as a barrier to entry, whereby competitors are hard-pressed to match the unit-cost advantages of handling bulky goods at this density. Secondly, capital efficiency is improving, with the inventory-to-revenue ratio tightening to 19%, signaling better turnover management.

3. Marginal Normalization and Marketplace Dynamics

The gross margins have discovered a “structural floor” in the 23-25% level. Although this is lower than the maximum level seen in 2023 with 26.8%, it is nevertheless the normalized level after integrating the previous acquisitions (Noble House Wondersign). The current margins are also impacted by “Abnormal Capacity” expenses: the startup costs to build additional storage facilities before reaching fully optimal volume efficiency.

The marketplace ecosystem is alive and well

Active Buyers: Registered a rise of 33.8% in their numbers to 11,419

Catalogue Depth: Goes beyond 50,000 SKUs, thereby achieving “Data Density” sufficient for optimal container filling.

Switching Costs: GCT has a strong “Pain of Exit”. It becomes quite difficult for a seller’s cumbersome inventory to switch to GCT after being absorbed into its physical infrastructure.

Final Exam

GigaCloud is a physical scale powerhouse masquerading as a technology platform. Having won the “logistics physics” in large-parcel goods, it is no longer a marketplace but mission-critical infrastructure for both the furniture and fitness industries. Debt-free, with an expanding global footprint, GCT is well positioned to absorb macro volatility while continuing to wear its crown as an “Efficiency King” in the B2B sector.

Final Thoughts: Where Growth Potential Meets Value Discipline

Having purged the noise from my own thinking, I am delighted to reach a clear conclusion: GigaCloud Technology is a rare species: it has a high-growth engine combined with a deep-value safety net. Although the “Achilles’ heel” of new tariffs may deter the rash speculator from entry, for the disciplined investor, it is in this very volatility of geopolitics that a generational opportunity emerges.

Why I’m Watching the coming days like a hawk:

The Growth Engine: With buyers active by 33.8% and revenues closing in on the billion dollar mark, GCT is essentially cornering the market in what they term ‘large parcel’ infrastructure. They’re selling furniture; they’re selling the only way to move it effectively.

The Value Fortress: It is difficult to find growth stocks with $334M in cash and no debt. The fact that management is buying back stocks in such large quantities is a strong message to the markets: they think the stock is undervalued.

Tariff Resilience GCT, being the ‘Efficiency Kings’, is better equipped than any other smaller firm to cope up or adjust to any new trade barrier. A trade war could even further expand its competitive advantage, as inefficient rivals would be weeded out.

The Verdict

If we witness signs of market weakness in the days ahead because of trade war stories in the headlines, I think of it as a “discount on the future.” GigaCloud is a dominant, asset-rich giant disguising itself in the form of a tech company platform. GCT is a contrarian buy for those who have a long-term vision and a value-oriented approach in mind because of this period of political uncertainty.

My Strategy: To accumulate on weakness. GigaCloud isn’t simply a trade; it’s a way of investing in the fundamental building blocks of global trade.

Brilliant analysis on the physical infrastrucure moat here. I've been tracking logistics-enabled marketplaces for a while and the switching costs you laid out are real, especially when you've got 10.9M sq ft of specialized racking that nobody else wants to replicate. The tariff angle actually strengthens their position since smaller players can't absorb the friction costs like GCT can.