I have owned Lululemon for a while. Personally I love their clothes, very comfortable, but also very expensive. I feel like its time to have a deeper look, after a couple off month of high volatility in the stock price. Even Dr. Michael Burry have invested in Lululemon. Are there still value in this company, and what about the growth story?

Lets dig in!

The Lululemon Evolution:

In the retail world, there are very few brands that have been able to harness the concept of “community” the way Lululemon has. From being a small design house in Vancouver, the company has grown into a massive entity that has redefined the entire concept of athleisure.

But as we enter early 2026, the firm now finds itself at a critical juncture. After a meteoric rise that led to record highs in late 2023, the last two years have been a tale of “growth normalization,” macro headwinds, and a gigantic valuation reset.

In this in-depth review, we examine Lululemon’s business model, their “Power of Three ×2” strategy, and what might have made the market so harsh to this retail darling lately.

1. Company Profile:

Be Human: Emphasize equity and inclusion in their worldwide supply chain.

Be Well: Supporting physical and mental well-being, working to overcome systemic inequity.

Be Planet: The use of sustainable materials and the concept of circularity (textile to textile recycling).

By embracing these values, Lululemon has fostered a “guest base” (they don’t refer to them as customers) that is arguably the most devoted in the sportswear business.

2. Strategic Framework: “Power of Three ×2”

The driving force for the expansion of Lululemon is the “Power of Three ×2” business plan. This business plan was introduced to achieve the goal of doubling the revenue for the year 2021 to $12.5 billion by 2026 through:

Product Innovation: Foraying into men’s wear (Steady State, ABC Lines), footwear (Blissfeel), and “net-new” experiences such as the Wundermost line.

Customer Experience: An “omni-operating model,” which combines 700+ physical locations with a huge digital footprint. Their membership offering, “Essentials,” now has over 17 million members in North America.

Market Development: A shift from being a predominantly North American company to a global brand, with a HUGE emphasis on China and the EMEA market.

3. The Stock price

The question is: Why Has the Price Fallen So Drastically?

Lululemon being a growing company, why did its stock price fall by almost half in 2025? The reasons lie in three key areas:

A. The “Americas” Stagnation. For several years, North America was the engine of growth. However, in the year 2025, comparable sales in the Americas became flat or slightly negative. This was a concern for investors, who thought the company had reached “peak saturation” in its domestic market.

B. The Margin Squeeze (Tariffs & Costs) With new trade tensions and the elimination of “ cheap imports” tax breaks, the cost of goods went up. With a company that takes great pride in its margins and a more conservative and inflation-skeptical consumer, Wall Street was spooked.

C. Leadership Transition: Towards the end of 2025, it was announced that Calvin McDonald, the CEO, would be stepping down in early 2026. This brought about “execution risk” during a period when the company is facing a tough retail market.

4. How They Make Money: The Omni-Channel Machine

The financial prowess of Lululemon can be attributed to their Direct-to-Consumer (DTC) business model. This allows them to earn more from their sales because they don’t rely on department stores for sales. Instead, they rely on their own retail stores and online platforms. This means they earn more

Gross Margins: Traditionally strong (55%-58%), but recently impacted by tariffs.

Revenue Mix: The Women’s category is still the focus, but Men’s and Accessories (bags, yoga mats) are the most rapidly growing categories in the revenue mix.

5. Global Markets: The Shift to the East

As the US market becomes more mature, Lululemon is now looking internationally. The results in 2024/2025 were staggering:

China Mainland: Growing at 67% year-over-year in the recent periods. China is no longer a side project; it is now the company’s primary growth engine.

EMEA Expansion: In 2026, Lululemon is entering six new markets, including India, Greece, Austria, and Poland, through a franchise business model to expand rapidly with less capital exposure.

6. The 2026 Outlook: Is the Bottom In?

Lululemon is starting 2026 as a “value play” rather than a “hyper-growth” stock. With the stock at its lowest valuation in years, the question for investors is whether the enormous growth in China can counter the slowdown in the US.

The company is still on track to meet its revenue target of $12.5 billion, but the journey to get there is no longer a straight one. For new subscribers who are considering the retail industry, Lululemon is the ultimate “brand power” case study: How does a strong brand retain its strength when the economic tides turn against it?

To grasp the current state of Lululemon, it’s necessary to move past the yoga mats and into the financials. In early 2026, we find ourselves in the presence of a remarkable and unusual market dynamic, namely a high-end, high-margin brand trading at “value” price points.

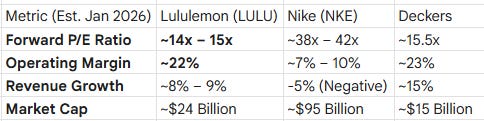

1. The Tale of the Tape: 2026 Valuation Comparison

Although Lululemon (LULU) has been forced to watch its multiples dramatically decrease, its competitors within the sport sector are being treated quite differently.

The “Nike Paradox”

The most telling piece of data is that Nike is currently trading at nearly 3x the valuation multiple of Lululemon, even though Nike has lower margins and is struggling with negative growth in its direct-to-consumer (DTC) channels. Investors are paying a premium for Nike’s “safety” and scale, while punishing Lululemon for its recent North American slowdown.

2. The “Multiple Compression”

“Multiple compression” is a another way of saying investors aren’t willing to pay as much for every dollar of Lululemon’s profit as they before were willing to due.

The Sentiment Shift: In 2021, investors were willing to pay 40 times earnings because they believed they would grow at 25% forever. But now, with the market at 14 times earnings, it’s as if the market is saying, “We only expect you to grow at the rate of the economy.”

If Lululemon is able to rekindle its North American market or continue its 60%+ growth in China, a “re-rating” (P/E ratio shifting from 14x to 20x-25x) could result in a huge stock price rebound.

3. The 2026 Catalyst: The CEO Search & NFL Move

Two major events are currently stabilizing the stock:

The CEO Transition: After Calvin McDonald’s departure, the industry is waiting for a new leader who can fill the gap between “lifestyle brand” and “performance powerhouse.”

The NFL Partnership: Lululemon’s latest foray into licensed NFL apparel is a direct attack on Nike’s turf. This is no longer just about yoga; it’s about dominating the multi-billion dollar “fan wear” market.

The Financials:

A fall of stock price like 2025 can be akin to a meltdown for investors. But when you examine the Balance Sheet and Operating Margins, the picture is actually very different. Lululemon is not a broken company it is a highly profitable machine that has been “put on sale” by the market.

1. The Balance Sheet: A “Zero-Debt”

With interest rates high and retail chains going bust, Lululemon’s balance sheet is an oddity.

Cash Position: As of the early part of 2026, Lululemon has about $1.0 billion cash and cash equivalents.

Zero Long-Term Debt: Lululemon continues to be one of the only publicly traded retailers in the world with no long-term debt. It gives the company “financial optionality,” meaning they do not have to borrow money from the bank in order to enter their six new markets in 2026, which include India and Poland.

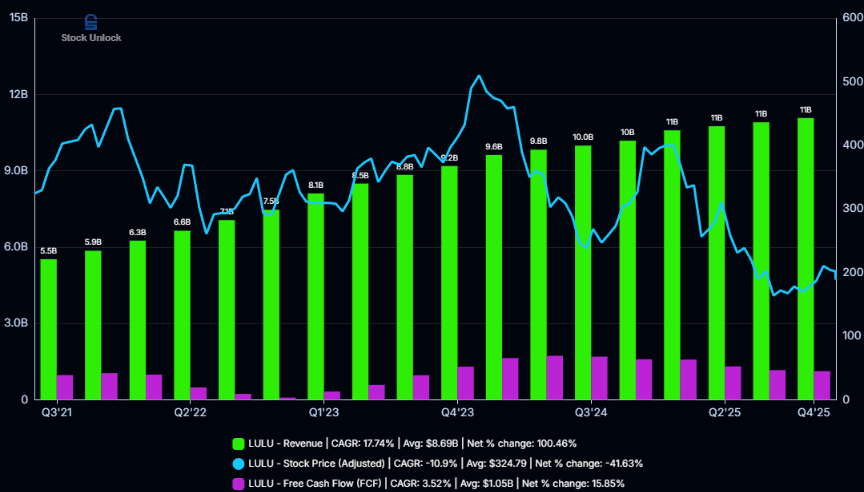

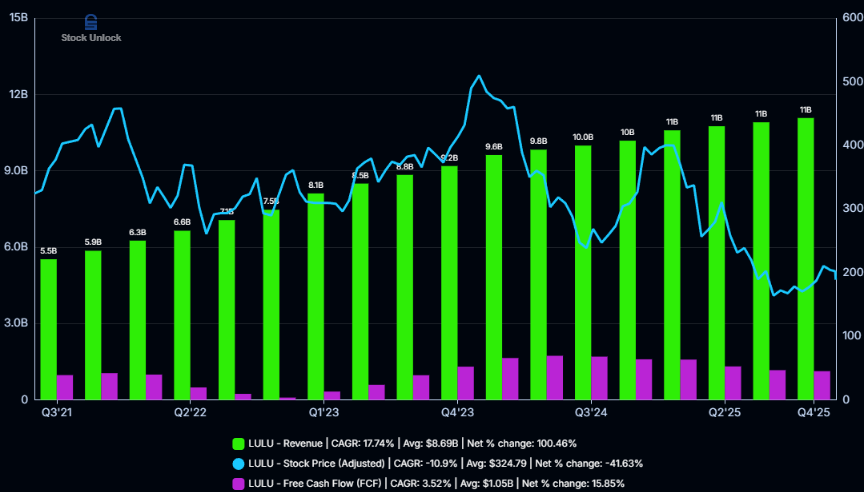

Inventory Management: One of the large “scare factors” in 2023-2024 was inventory growth. As of Q3 2025, inventory units are only 4% year-over-year growth, showing that the management is back in control of their supply chain.

2. The Margin Story: Industry-Leading “Pricing Power”

Looking at The “moat” of any retail brand is its ability to sell products at full price without constant discounting. Despite the recent macro pressures, Lululemon’s margins remain the envy of the entire retail brand industry.

The “Tariff” Note that while gross margins ticked lower late in 2025 due to new trade tariffs and the elimination of “cheap imports” tax exemptions, Lululemon has already started shifting production to lower-cost regions to defend these margins for the 2026-2027 fiscal years.

3. The ‘Aggressive Buyer’ Reason: Share Repurchases

“So cheap” yet not buying back stock. Yet, they are. In December 2025, the Board of Directors approved an enormous increase of $1.0 billion to their stock repurchase program. Currently, they have about $1.6 billion remaining for purchasing their stock.

Takeaway: A firm that finds itself in $1B cash and debt-free and chooses to buy back stock in a aggressive manner at the current valuation multiple of 14x must mean that the folks running the firm know that the market’s assessment on valuation is incorrect.

Summary: 3 Reasons to “Buy the Dip” in 2026

Valuation vs. History: Lululemon historically traded at 35x-40x earnings. Today, you are buying that same brand power at 13.8x - 15x. You are essentially getting a premium brand at a “supermarket” price. A reason for this is the slowdown in US growth, but i do believe that with a new CEO coming, and a strong focus on this. They will be able to get some growth back.

The China Engine: International revenue grew 33% in Q3 2025. While the US is “slow,” China growth is exploding. Lululemon is successfully changing from a “North American Brand” to a “Global Staple.”

Capital Efficiency: Because they have no debt and high cash flow, every dollar of growth in China goes straight to the bottom line (and eventually back to shareholders via buybacks).

My final verdict and why i own this stock

The picture as we wrap up this analysis into early 2026 consists of fundamental strength vs. sentiment weakness. Right now, the market is treating Lululemon as a “legacy” retailer, but the internal numbers are telling a different story: that it remains a high-performance growth engine.

Key Findings: The Balance Sheet is a Fortress: With zero long-term debt and more than $1 billion in cash, Lululemon has the “antifragility” to withstand a US recession while at the same time funding global expansion aggressively. Efficiency is king: Operating margins near 20% and gross margins at 58% are nearly double those of Nike. This is a high-margin luxury brand masquerading as an apparel company.

The 2026 Catalysts: Why Now?

The following 12 months are full of events that could cause the company’s stock to re-rate:

New Leadership: The search for new CEO Calvin McDonald’s replacement is seeing completion. Hiring a heavy hitter would help investor confidence in US growth.

The India Entry: In 2026, Lululemon is making a formal entry into the Indian market. With the success in the Chinese market, where it is seeing a 60%+ increase, the Indian middle-class rise is the next big opportunity.

Activist Pressure: With the reported stake of Elliott Management in 2025, the pressure for managing the cost structure better and distributing even more capital to the shareholder base grows.

To invest in Lululemon at the current juncture is not to invest in yoga pants. No, it is to invest in capital allocation. You are essentially investing in a company that is rolling in cash, has no debt, and is purchasing its own stock at a bargain. This is typically the formula for success in the retail industry.

Thanks for reading! Feel free to make a comment, if you have some views about the company that I might have missed. Also, please share and subscribe to help grow the community

I like the lowercased "i"s throughout, less of an AI feel ha

Writing in another language sometimes takes time to master I guess… haha!