As my quest for look closer to European companies I have stumbled upon Norbit ASA, which I believe very soon will be apart of my portfolio. This is not a turnaround case but a growth case with the correct setup for the current market.

This could be a multibagger going forward, even though the stock already is up 471% over the last 3 years. There is no sign the stock is close to being done with this movement.

The Norwegian Niche Sniper: How Norbit ASA is Beating the Tech Giants

While the world’s attention is fixated on the “Magnificent Seven” and the latest and greatest in AI software, a little-known engineering marvel in Trondheim, Norway, has been flying under the radar, achieving triple-digit earnings growth by dominating the world’s toughest “small” markets.

If you don’t know who they are, it’s because they don’t make smartphones or social media apps. They make the specialized, high-precision equipment the world’s most critical industries literally can’t function without. They are the ultimate “Niche Sniper”: they help map the “forgotten” floor of our oceans, as well as track millions of trucks moving across the borders of Europe.

What is Norbit ASA?

In short, they are a technology specialist. They don’t just make hardware; they make ultra-niche sensors and connectivity products where precision is more important than price.

They exist in a world where there are “high barriers to entry.” You can’t just start a sonar business in your garage, and you can’t just replace the digital tachograph in a truck with something else. This gives them a “moat” effect, which allows them to make margins that most hardware businesses would kill for.

How do they actually make money?

Norbit makes money through three different “engines,” and they are different for different parts of the portfolio.

The ‘Oceans’ Engine (High-Margin Proprietary Tech): This is their jewel. Norbit creates the world’s most compact, high-resolution sonars used for seabed mapping and building offshore wind farms. For every new offshore wind farm built in the North Sea or harbor dredged in Asia, there is a high probability a Norbit sonar is ‘looking’ at what is going on underwater. The Profit Model: They own the Intellectual Property. They sell very expensive pieces with an EBIT margin above 30%.

Connectivity” Engine (Recurring & Regulatory Demand): If you’re a truck driver in Europe, chances are you’re carrying Norbit technology. They provide the hardware for electronic tolling and “Smart Tachographs” – devices that monitor drivers’ hours.

Profit Model: This is due to government regulation. When the EU changes regulations on how trucks have to be tracked, millions of them have to be upgraded. This is a huge, predictable cycle of replacement demand.,

The “PIR” Engine (The Defense & Security Catalyst): Product Innovation & Realization (PIR) is where they assist other companies and now Defense Departments in manufacturing complex electronics.

The Profit Model: This section has recently seen explosive growth (nearly 100% growth in 2025) due to huge defense contracts. They utilize their high-speed, automated factories in Norway to assemble the “guts” of modern security and defense systems.

I believe their business model is very relevant in many places, both with Green energy in Europe, and also the massive defense budget Europe is going to deploy over the coming years.

The competition - Why Norbit wins the battle

If you’re deciding between the maritime titans, chances are you’re looking at Kongsberg Gruppen (KOG) or Teledyne (TDY). But for a growth-oriented investor, there’s something that Norbit brings to the table that those titans cannot: Agility and Capital Efficiency.

1. The “Return on Equity” (ROE) Gap

Norbit posted an astonishing “Return on Equity” (ROE) of 30% in 2025. To illustrate the point, while Kongsberg is an incredible company, its size makes it difficult to “move the needle” with a single contract. Norbit, on the other hand, is in its “sweet spot” in terms of size: large enough to have the manufacturing capabilities to fulfill a single NOK 120 million defense deal (which they signed in late 2025), but small enough that it can “move the needle” with a single such contract.

Going forward winning these contracts will prove that they are able to be a serious competitor in the defense segment. I do believe this could be a possible catalyst going forward.

2. Profitable Niche Dominance vs. “Bloated” Rivals

Consider the Connectivity industry. Norbit’s chief competitor, Kapsch TrafficCom, has been engrossed in the past two years in costly lawsuits and low-margin infrastructure contracts, with EBIT margins stuck in the low single digits (2-5%).

The Norbit Edge: By exclusively targeting high-margin hardware (the “brains” of the tolling systems) and not the “dirt and gravel” of infrastructure construction, Norbit sustains EBIT margins of 25% or better. They are, in essence, the “Apple” of the trucking technology industry: they control the high-margin hardware and outsource the low-margin labor.

3. The “Shareholder-First” Catalyst

Unlike most growth tech stocks that burn cash for years, Norbit is a true Cash Machine.

The Icing on the Cake: In November 2025, not only did the company pay their normal dividend but also paid an extraordinary dividend of NOK 3.00 per share.

Why own this stock? You are getting a growth tech stock with 40%+ revenue growth from the Oceans segment and a 3-4% dividend yield while you wait for the next breakout.

The Bottom Line: You are a Norbit shareholder because you want access to the Defense Boom and Offshore Wind growth themes without the “conglomerate discount.” Norbit is a pure play on high-precision engineering with a management team fixated on return on capital.

The Financial Engine: From “High Growth” to “High-Yield”

While 2023 may have been the year Norbit showed the world it could scale, 2025 has been the year it showed the world it could dominate. Norbit has moved from being a “small cap story” to being in the midst of massive capital return.

1. The Numbers: Top-Line Acceleration

Although the 30% growth in 2023 was quite impressive, the trend has only accelerated. Norbit has managed to pack three years of growth into eighteen months.

2. DuPont Analysis: Dissecting the 30% ROE of Norbit

In order to understand why Norbit is a “quality” stock, one has to understand their ROE. As of early 2026, Norbit has an ROE of 30.2%, which is nearly triple the industry average of 10.9% for the electronic industry.

This can be broken into three different “gears”:

Net Profit Margin (16.7%): This is the “Pricing Power” gear. Despite the rise of global inflation, Norbit’s proprietary technology in the Oceans segment has them maintaining an industry-high 35%+ margins for their overall net profit margin.

Asset Turnover (1.1x): This is the “Efficiency” gear. Norbit is running its Norwegian factories at full capacity. They are turning over their total assets more than once a year a rare achievement for a hardware-intensive business.

Financial Leverage (2.0x): This is the “Safety” gear. Norbit is not “faking” their returns by using risky debt because of their 50% equity ratio. They are using just enough leverage to increase returns without jeopardizing their balance sheet.

3. The “Cash-Rich” Capital Allocation

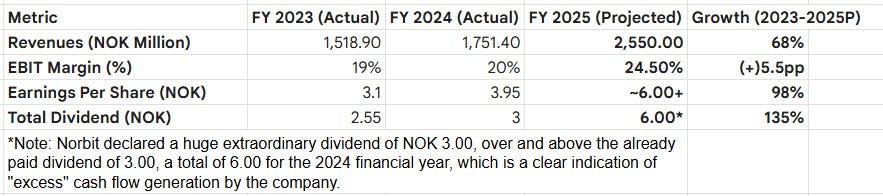

The single biggest change since 2023 is the board’s aggression. They are no longer “protecting” the balance sheet; they are optimizing it. By paying out NOK 6.00 in total dividends in 2025, they are signaling to the market that the business is now a “cash machine” and is able to fund its own R&D while paying shareholders a level of dividend more commonly seen in mature oil or tobacco companies.

Why This Matters for the Long-Term Investor.

Norbit has made the transition. You are no longer buying a promise of future profits. You are buying a company that:

Reinvests at 30% ROE.

Grows at 40% per annum.

Pays a dividend yield that competes with High-Interest Savings Accounts.

This final section deals with what is arguably the most important variable for any global tech investor: Currency Risk. For a firm like Norbit, which is headquartered in Norway but serves the entire world, the exchange rate is not a trivial consideration—it’s a huge determinant of the bottom line.

The “Krone” Factor: How to Handle the Double-Edged FX Sword in “Krone”-Reporting Norbit

As of the early part of 2026, Norbit is still a “Currency Play” as well as a “Tech Play.” Since the company files its earnings in Norwegian Krone (NOK) but derives over 90% of its revenue in USD and EUR, the Krone’s volatility can make a “good” quarter look “great” – or a “great” quarter look “mediocre.” I’m not going to act to be an expert in the FX segment, but this is a spot to keep a look at.

Insider ownership

The CEO is the Top Shareholder

Currently, as of early 2026, Per Jørgen Weisethaunet, the company’s CEO, is its biggest shareholder by individuals. He does so through his holding company, PETORS AS, which holds 10.9% of the total shares

The founder of the company, Steffen Kirknes, has, in recent times, transferred some of his stakes to a family office for diversification purposes (Draupnir Invest; however, he still retains the position of the second-largest shareholder through VHF Invest AS, which owns 9.6% equity

The Reitan Family (9.5%) — one of Norway’s most successful industrial families.

The conclusion is a there is a great sign of “Skin in the game” which we like to see in this size of a company.

The final take

Disciplined investors should prioritize their main investment thesis over a laundry list of less significant catalysts. A “North Star” gives an investment the necessary conviction to stay the course through volatility, while a laundry list of catalysts indicates a lack of understanding of the stock.

First and foremost, there are enormous reasons to invest in NORBIT due to its extraordinary “operating leverage” - whereby the bottom line is currently being supercharged. While the company has exhibited a respectable 23% revenue growth CAGR in the five-year period between 2019 and 2023, there has been something more phenomenal happening behind the scenes with last year’s 30% growth in revenues - accompanied by an explosion in Earnings per Share (”EPS”) growth by 71% last year alone, rising from NOK 1.82 to NOK 3.10. This is not a growth story - this is an acceleration story. This is not the same company as two years ago - every extra krone of revenues is now delivering a far higher level of profit for the company.

Norbit ASA is a rare combination: high-velocity growth, accelerating profitability, and a management team confident enough to issue extraordinary dividends.

It will be a successful investment if the Oceans and Connectivity segments continue with double-digit momentum. However, my conviction is pegged to the efficiency of the engine. The 60% gross margin is the new high-water mark. If we see a sustained retreat back toward the high 40s, or if employee expenses begin to swallow the gains from revenue growth, the thesis is broken and it’s time to exit. As things stand, the operational leverage remains the most compelling story in the niche tech landscape. Maintain high-conviction “Buy” as long as the 60% margin floor holds.

The stock has seen a big rise in the share price but I don’t believe it’s done just yet.