Sezzle Inc. (SEZL) Deep Dive

Triple-digit returns or regulatory time bomb? Why I’m Keeping this fintech star on my watchlist.

The Sezzle Deep Dive:

January 7,

Company name: Sezzle Inc.

Ticker: SEZL

Market cap: $2.22B

Stock price: $72.05

If you’re looking for a 30-page institutional deep dive, you won’t find it here. This is a high conviction dissection of the business distilling exactly what you need to know and ignoring the noise. If you value this type of objective analysis, please subscribe and share to help grow our community.

In the world of fintech, stories of “growth at all costs” are common. Stories of a company staring into the abyss of a 90% share price collapse, only to emerge as a highly profitable, cash-generating machine, are rare. Sezzle is that rare story.

Once dismissed as a minor player in the shadow of giants like Klarna and Affirm, Sezzle has “flipped the script” on the traditional BNPL(Buy now pay later) model. As of the Q3 2025 results, the company has transitioned from a merchant-dependent payment button to a high-margin, consumer centric financial ecosystem.

Part one: The history

1. A tale of two companies

Sezzle’s history is best understood as two distinct eras: The Expansion Era (2016–2021) and The Efficiency Era (2022–Present).

The Expansion Era: Founded in 2016, Sezzle followed the standard fintech playbook: raise capital, pursue Gross Merchandise Volume (GMV) at any cost, and expand globally. By late 2021, however, rising interest rates and a failed merger with Zip Co. left Sezzle with a massive burn rate and a tanking valuation.

The Strategic Pivot: In 2022, management made a brutal but necessary choice: they abandoned the “growth at any cost” mantra. They shuttered international operations, slashed headcount, and focused exclusively on the US and Canadian markets.

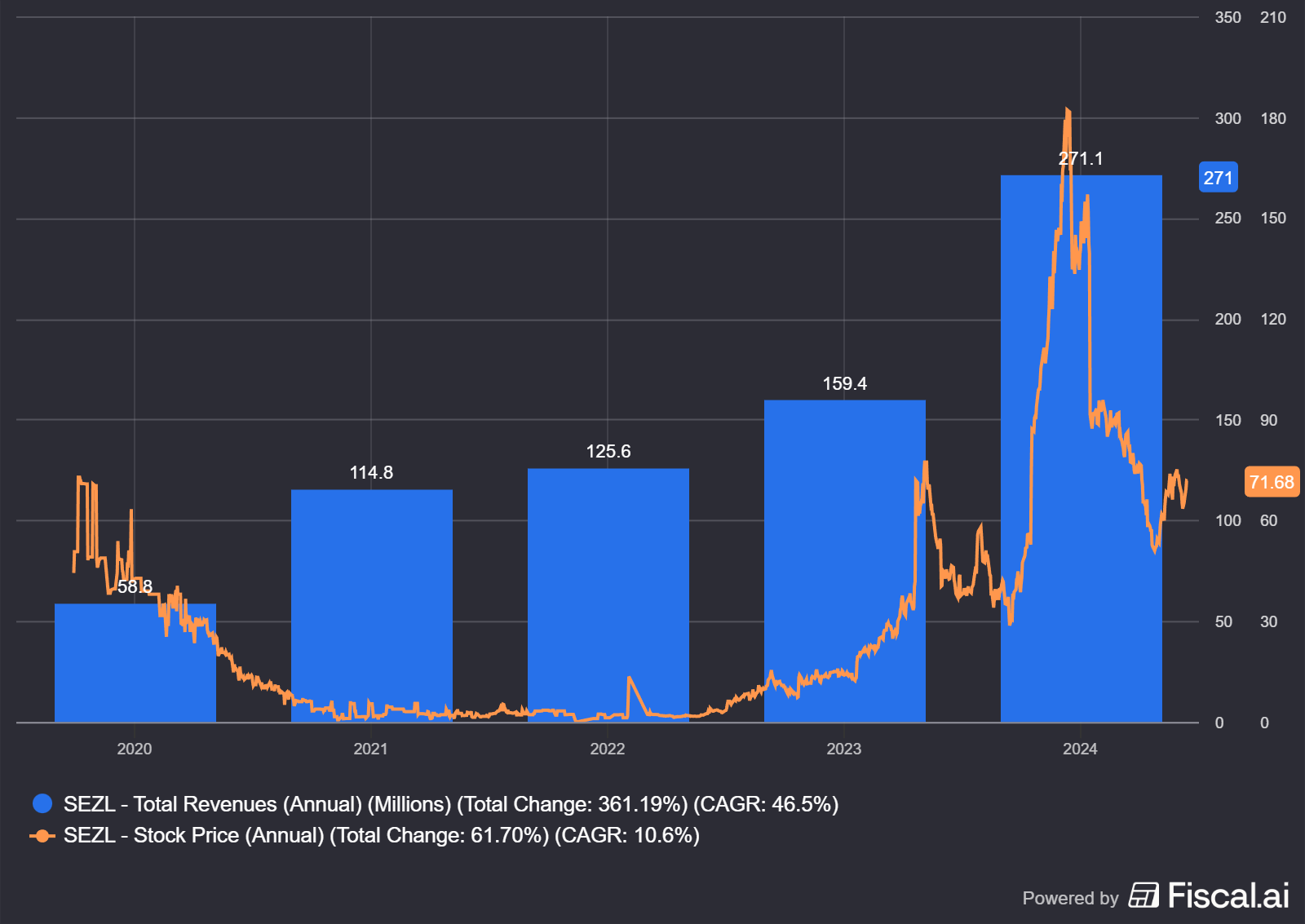

The Resurgence: In 2023, Sezzle moved its primary listing to the Nasdaq. More importantly, they achieved something their larger peers struggled with: sustained GAAP profitability. Today, Sezzle isn’t just a payment option; it’s an efficient financial engine.

2. How Sezzle makes money: The three headed revenue monster

Unlike traditional BNPL players that rely almost exclusively on merchant fees, Sezzle has diversified into a “consumer-sided” model. Based on the latest Q3 2025 data, their revenue streams are split into three key areas:

A. Merchant fees (The core foundation)

This is the traditional BNPL revenue. When a user buys a product at a partnered merchant, the merchant pays Sezzle a fee (typically 3–6%). Sezzle takes the credit risk, pays the merchant upfront, and collects from the consumer over four installments.

B. The subscription engine (The SaaS transformation)

This is Sezzle’s “secret sauce.” They have introduced two tiers that have transformed their unit economics:

Sezzle Premium & Sezzle Anywhere: These subscription products allow users to use Sezzle at non partnered brands (like Amazon or Target) or anywhere Visa is accepted.

High Margin Growth: As highlighted in the 3Q25 Presentation, the growth in Monthly On-Demand Subscribers (MODS) is a key driver of their valuation. These subscriptions provide recurring, high-margin revenue that is independent of specific merchant partnerships.

C. Consumer fees & value added services

Sezzle earns fees for failed payments and for “Sezzle Up,” a feature that allows users to report their payment history to credit bureaus. This “Financial Wellness” angle attracts a specific demographic looking to build credit, creating high user stickiness and lowering customer acquisition costs.

3. Where the company stands today: Operational excellence

As of late 2025, Sezzle is no longer a “distressed” play; it is a high yield financial operator.

The Inflection Point: The Q3 2025 results confirm a trend of “Operational Leverage” where revenue grows significantly faster than operating expenses. This has led to record high Net Income margins for the sector.

Aggressive Capital Allocation: In a major show of confidence, Sezzle has continued its aggressive Share Buyback Program. By reducing the share count while earnings explode, the company is dramatically increasing its Earnings Per Share (EPS), a classic “Deep Value” move.

Risk Management: Despite the subprime label often attached to BNPL, Sezzle’s Provision for Credit Losses remains tightly managed. Their short duration loans (6 weeks) allow them to adjust their “credit spigot” almost instantly in response to macro economic shifts.

Part 2: The BNPL industry

To understand Sezzle’s potential, one must first understand the ocean it swims in. The BNPL industry has often been dismissed as a “low interest rate phenomenon,” yet the data suggests a permanent structural shift in how North Americans manage their wallets.

1. The macro view: A 2% penetration with massive upside

Despite the headlines, BNPL is still in its infancy in North America. Currently, BNPL and POS financing represent less than 2% of the total commerce transaction value in the region.

The Growth Gap: While credit and debit card usage is projected to remain flat or even decline slightly in CAGR through 2030, the BNPL market in North America is expected to grow at a 12.9% CAGR from 2024 to 2030.

The Market Opportunity: The total North American BNPL market size was estimated at $257 billion in 2024, split almost evenly between online and in-store financing.

Market Share: Sezzle currently holds approximately 1% of this total BNPL market, leaving a vast “blue ocean” for expansion as they move beyond niche e-commerce into everyday spending.

2. Demographic Tailwinds: The “Credit Invisible” opportunity

Sezzle isn’t just competing for existing credit card users; they are capturing a demographic that the traditional banking system has left behind.

The “Invisible” Market: There are 49 million adults in the U.S. who are either “credit invisible” or unscoreable.

Generational Shift: Younger generations (Gen Z and Millennials) have significantly lower average FICO scores compared to Baby Boomers, yet they are the primary drivers of future consumption. Approximately one third of Sezzle’s consumers are Gen Z or Millennials.

The “Sezzle Up” Advantage: By offering credit reporting through Sezzle Up, the company has turned a payment tool into a “financial wellness” product. This creates a powerful incentive for users to pay on time, resulting in a 97% repeat customer usage rate as of Q3 2025.

3. Future frontiers: Beyond the checkout button

The Q3 2025 roadmap signals that Sezzle is evolving into a full scale digital bank.

Omnichannel Domination: With 37% of “Anywhere” orders now occurring in-store, Sezzle is successfully moving off the screen and into the physical world.

The “Fintech Super-App”: New features launched in 2025 including Sezzle Arcade, Money IQ, and a beta for Pay-in-5 are designed to increase “Monthly Sessions,” which grew 78% YoY as of September 2025.

Bank Partnership: Their strategic 5-year partnership with WebBank (launched in late 2024) allows for a more streamlined regulatory approach and provides the rails for future products like Sezzle Balance and checking accounts.

Part 3: The financial engine — high velocity, high returns.

If you look at Sezzle’s headline numbers from the Q3 2025 results, they seem almost “too good to be true” for a lending business. A 107.0% Return on Equity (ROE) and a 22.8% Net Income Margin are figures usually reserved for capital-light software companies, not firms that facilitate billions in credit.

To understand how they do it, we have to look through the lens of the DuPont Analysis.

1. The DuPont breakdown: The anatomy of 107% ROE

Traditional banks generate ROE by taking massive leverage on thin margins. Sezzle does the opposite. Their 107% LTM ROE is driven by three distinct levers:

Elite Profitability (Net Margin): With a 22.8% GAAP Net Income Margin, Sezzle keeps nearly a quarter of every dollar it earns after all expenses and taxes. This is driven by their “Subscription Pivot”—moving from low-margin merchant fees to high-margin recurring revenue.

Hyper-Velocity (Asset Turnover): This is the most misunderstood part of the Sezzle case. Unlike a bank with 30-year mortgages or 5-year auto loans, Sezzle’s average loan duration is just 42 days. This means they can “turn over” their capital nearly 9 times a year. High velocity allows them to generate massive volume (GMV) with a relatively small balance sheet.

Smart Leverage (Equity Multiplier): Sezzle uses warehouse credit facilities (like their partnership with WebBank) to fund their receivables. Because their loans are so short-term and their margins so high, they can use debt effectively without the typical “blow-up” risk of long-dated subprime lenders.

2. The balance sheet: clean and lean

One of the biggest “Red Flags” for Value Investors is a balance sheet bloated with “Intangibles” or “Goodwill.” Sezzle’s balance sheet is refreshingly focused on Short-term receivables.

The “Provision” shield: As of Q3 2025, Sezzle’s provision for credit losses is tightly managed as a percentage of GMV. Because they see repayment trends within 14 days, they can “turn off the tap” for risky borrowers almost instantly if they see the economy softening.

The buyback signal: In 2024 and 2025, Sezzle completed a $20M repurchase and announced an additional $50M program. For a “growth” company to aggressively buy back its own shares suggests that management believes the market is fundamentally mispricing their future cash flows.

3. Management & founder alignment: skin in the game

A “Deep Dive” is never complete without looking at who is at the helm. Sezzle is still led by its co-founders, Charlie Youakim (CEO) and Paul Paradis.

Founder Ownership: A critical “green flag” for Sezzle is the exceptionally high level of Founder/Insider Ownership. Charlie Youakim, in particular, remains one of the largest shareholders. This high degree of “skin in the game” aligns management’s interests directly with common shareholders. They aren’t just employees; they are owners who felt the pain of the 2022 crash and are now reaping the rewards of the pivot.

The “Public Benefit” Mission: Sezzle is a Certified B Corp (or operates with a Public Benefit purpose). While some analysts dismiss this as “ESG noise,” for Sezzle, it is a customer acquisition tool. By positioning themselves as the “Responsible Way to Pay” and helping users build credit, they lower their churn and increase user LTV (Lifetime Value).

4. The Growth Case: What happens next?

Where does Sezzle go from here? The Q3 2025 Presentation outlines a clear path:

Subscriber Scaling: Moving more of their 18M+ sign-ups into the Anywhere/Premium tiers.

Product Expansion: The beta testing of Pay-in-5 and the launch of Sezzle Arcade suggest they are building an ecosystem where users stay inside the Sezzle app for more than just a single purchase.

The “Bank” Evolution: With WebBank as a long-term partner , the roadmap toward a “Sezzle Checking Account” or “Sezzle Credit Card” is now a reality, not just a pitch deck dream.

Part 4: Stress testing the Sezzle thesis

In every “Deep Value” case, the greatest danger is confusing a cyclical peak with a structural breakthrough. Sezzle has undeniably executed a brilliant pivot, but as we move into 2026, three “Black Swan” risks loom over the horizon.

1. The regulatory guillotine (CFPB)

The BNPL industry is currently operating in a “regulatory gray zone.” The Consumer Financial Protection Bureau (CFPB) has signaled that it intends to treat BNPL providers more like traditional credit card companies.

The Risk: If Sezzle is forced to implement more rigorous (and expensive) credit checks or faces a cap on “service fees,” their high margin subscription model could be decimated.

The Impact: Increased compliance costs and lower fee income would compress those 22.8% net margins back toward thin, bank-like levels.

2. The credit cliff: Subprime sensitivity

Sezzle’s primary demographic is the “credit invisible” or those with below-average FICO scores.

The Risk: In a “Soft Landing” economy, Sezzle thrives. However, in a true recession with rising unemployment, the BNPL bill is often the first one consumers stop paying. Because these are small-ticket, unsecured loans, the legal cost of recovery often exceeds the debt itself.

The Hard Fact: While their current Provision for Credit Losses is managed, a spike in “bad debts” (consumer defaults) is the fastest way to wipe out equity in a high-velocity business.

3. The moat-less commodity

At its core, Sezzle provides “money for a fee.” This is a commodity.

The Competition: When Sezzle was small, the Goliaths (JPMorgan, Apple, Affirm) ignored them. Now that Sezzle is showing 100%+ ROE, they have a target on their back. If a major bank integrates a “Pay-in-4” feature directly into their checking accounts with zero fees, Sezzle’s “Anywhere” subscription loses its primary value proposition.

My final take: A quality business at a crossroads

I’m keeping Sezzle on my watch list, but I’m not hitting the “buy” button just yet. From my perspective, this is a HOLD. Here is why: although the short term numbers are spectacular, the 10-year horizon for BNPL is clouded by inevitable regulatory tightening. History shows that when companies move this fast in the credit space, the “regulatory hammer” eventually drops. I’m looking for a deeper discount to account for this long-term policy risk. If we see a further drop in price that provides a true cushion against these uncertainties, I’ll reconsider, but for now, I’m observing from the dugout.

Thanks for reading don’t forget to share and subscribe!

Disclaimer & Disclosure

Not Investment Advice: This report is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. The information and analysis contained herein represent the subjective opinions of the author and should not be interpreted as a recommendation to buy, sell, or hold any security.

Accuracy of Information: While i have made every effort to ensure the accuracy of the data presented utilizing publicly available information, including Sezzle Inc.’s Q3 2025 financial reports and investor presentations all information is provided “as is” without warranty of any kind. Financial markets are dynamic, and data can become outdated or subject to revision.

Really enjoyed this deep dive. Great to go deeper on the business it’s clearly very well managed. Excellent work.