Technoglass Inc. (TGLS)

Why the market is dead wrong about the Colombian Glass King

January 12,

Company name: Technoglass Inc.

Ticker: TGLS

Market cap: $2.34B

Stock price: $53.68

I have been looking around for stable companies, undergoing some headwind due to a current situation that could be overblown. And up came Technoglass Inc.

Lately they have been through a short-seller attack and allegations of some shady Colombian Connections. The result of that? the stock dropped almost 50%.

Sounds pretty bad right? Maybe? Let’s find out.

Disclaimer: This is not a 60 page deep dive, guess what? you don’t need a 60 page deep dive to understand this case.

First let me give you some insight about Techoglass.

As they put it on their website “Tecnoglass is a leading manufacturer of architectural glass and associated aluminium and vinyl products for the global commercial and residential construction industries”. Based in Barranquilla, Columbia, although they mainly operate in the US, with the biggest market in Florida.

Technoglass operates in Colombia, which gives them a real edge because labor costs there are way lower compared to what US companies deal with back home. This setup results in margins over 40%. While the competitors operate with margins around 25%. At the same time production has been mastered, cutting the production time almost in half from what the competition operates with.

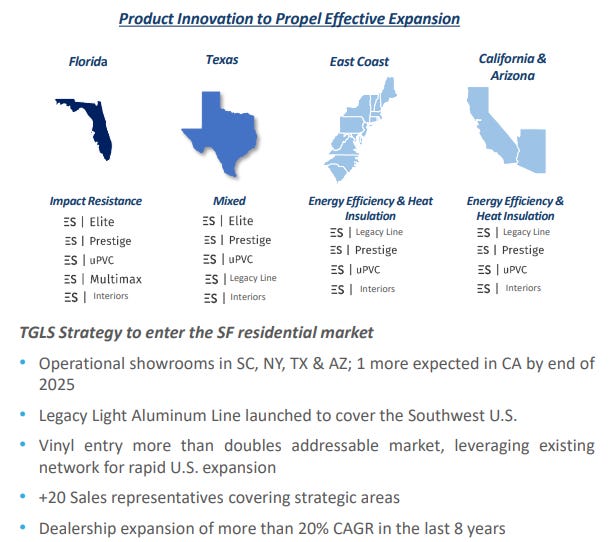

Most of today’s revenue comes from the US (95%). Florida is today the mail spot, but expansions towards Texas and California are well underway.

For a long time, the company focused on aluminum products. Aluminum works fine in warm places like Florida, I think. But to reach more of the US, especially colder areas, they realized vinyl was necessary.

So in late 2024 and into 2025, they started rolling out vinyl window lines pretty aggressively. This change is not minor, it basically doubles the total addressable market from 13 billion to over 26 billion dollars. Early signs show it working, with residential sales picking up share in those colder climates where vinyl tends to dominate. The margins part stands out here, since it ties back to their cost advantages.

Revenue Potential: Once these lines are fully ramped up, management expects them to add approximately $300 million in annual revenues.

The current operational Status: The ramp up is already gaining momentum. The company is leveraging its existing network of roughly 60 legacy dealers in Florida who were already selling both aluminum and vinyl products from other suppliers. This "plug-and-play" strategy allows for a much faster sales ramp than building a dealer network from scratch.

Just like their aluminum business, Tecnoglass is applying its vertically integrated model to vinyl. They leverage their existing manufacturing expertise to retain profit at every step of the production process. By producing vinyl profiles and windows in their low cost Colombian hub, they can offer high spec, energy efficient products at prices their U.S. competitors who often have much higher labor and overhead costs simply cannot match.

The Vinyl part will turn the company into a diversified national building products powerhouse, with top of class margins.

The vinyl expansion is the engine that will likely drive the company's goal of double-digit revenue growth in 2026. It provides a natural hedge against regional slowdowns in Florida and allows them to capture the growing demand for green, energy-efficient building materials.

The Financials

The stock price has been volatile, but the fundamentals are pointing to great growth. In Q3 2025, Tecnoglass reported $260.5 million in revenue, up 9.3% year-over-year.

The backlog thing stands out more though. They have this huge one now, a record 1.3 billion dollars. It increased by 21.4 percent compared to last year. This means they know what is coming in for the next year and a half or so. Especially since the commercial part is a big chunk, sitting at 60 percent of their revenues.

On the balance sheet, not many companies in this area are doing great with the high interest rates. But Tecnoglass seems strong.

They have more cash than debt, basically a net cash position. The ratio of net debt to their last twelve months adjusted EBITDA is negative 0.04 times, which I think shows they are not stressed about money.

Liquidity is around 550 million dollars total. That includes 124 million in actual cash.

They just bumped up their share buyback to 150 million dollars. Management must believe the stock is too cheap right now.

For someone investing, this points to a solid business that makes cash from how it runs things. Not from taking on too much debt or risks. It feels like the operations are the key here. Some might worry about the volatility, but the backlog covers that for now.

Lets return to the issues:

Now, let’s talk about the elephant in the room. In August 2025, a short-seller report from Culper Research hit the stock hard, alleging past ties to drug cartels and questioning the legitimacy of their financials.

Tecnoglass didn’t just ignore it. They hired Alex Spiro (the high-profile attorney known for representing Elon Musk) and filed a defamation lawsuit. The company has been vocal that the allegations are based on “fabricated” and “inauthentic” documents, a claim they state has been backed by the Mexican government.

When they take this to the federal court in New York, it suggests they have nothing to hide. There has been a voluntary dismissal without prejudice noted in late 2025, which will often signal a procedural move or a potential settlement. I’ll be watching this very closely in early 2026.

But if they did not fight back I would look very wrong, the founding owners, the Deas brothers currently own 43% of the company. This alignment of interests is exactly what you want when a company is under fire.

The Final take

Currently we are facing a company with great growth, expansions to new markets, under a lot of “drama” pressure. Yes if the reports hold up, it could be bad for business ahead, with mistrust. But if the news blows over, with no specific hold up in court, you now have a great opportunity to purchase a growth industrial king at a discount. Average analysts have a price target of 75$ about +40% from current levels.

Check out Fiscal AI for a great research tool! Click here!